India’s Fall in the Global Market Hierarchy

How much more can the Indian stock market afford to lose its position in the global market capitalisation rankings?

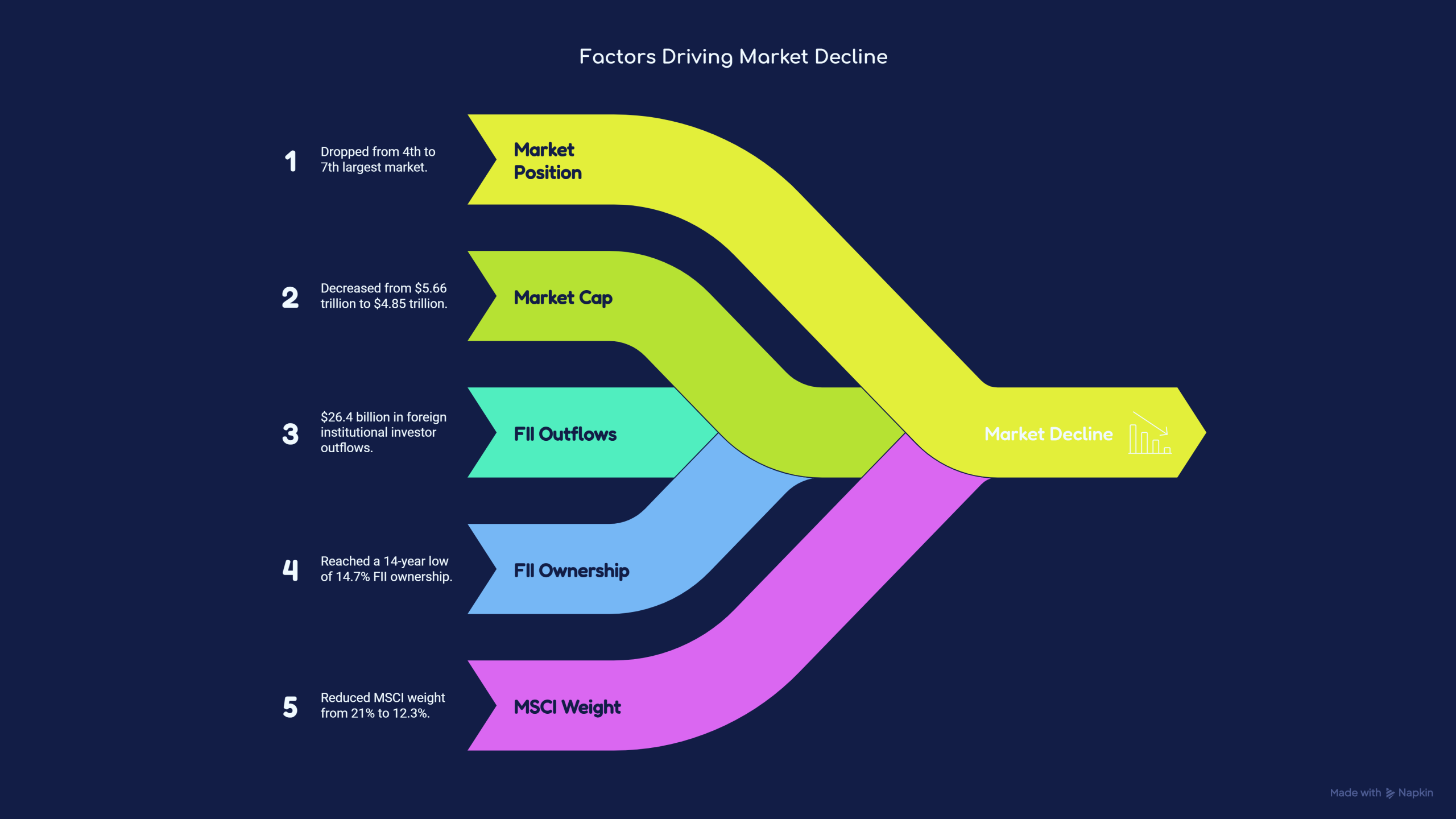

The question may sound alarmist, but recent developments suggest it deserves serious consideration. India, which only recently emerged as the world’s fourth-largest stock market, has now slipped to the seventh position in global market capitalisation rankings. Taiwan and South Korea have moved ahead, driven by a powerful rally in technology and semiconductor stocks, while India has struggled with persistent foreign investor selling, slowing earnings growth and valuation concerns. India’s total market capitalisation, which touched nearly $5.66 trillion in September 2024, has now fallen to around $4.85 trillion, wiping out almost $800 billion in market value. While market rankings fluctuate over time, India’s decline raises an important question: are foreign investors losing confidence in India, or are they merely waiting for better opportunities?

The Great Foreign Investor Retreat

Foreign Institutional Investors have been one of the most important drivers of Indian equity markets for nearly three decades. Their investment decisions influence liquidity, valuation multiples and investor sentiment. Over the last ten months, FIIs have withdrawn more than $25 billion from Indian equities, making the current phase one of the most significant periods of foreign selling in recent history. The impact of this withdrawal extends beyond stock prices. Foreign ownership in listed Indian companies has fallen to approximately 14.7 percent, the lowest level in nearly fourteen years. A decade ago, foreign investors owned close to 20 percent of Indian equities. This sharp decline suggests that the current selling pressure is not merely a short-term reaction but part of a broader reassessment of India’s investment attractiveness.

Yet, despite this exodus, Indian markets have not collapsed. This itself is a remarkable development. Domestic institutional investors have steadily absorbed much of the foreign selling. Today, domestic institutions own nearly 19 percent of Indian equities, surpassing foreign investors for the first time in India’s market history. The rise of mutual funds, SIP investments, insurance funds and pension money has fundamentally changed the structure of Indian capital markets.

What History Tells Us About FII Behavior

To understand when FIIs might return, it is useful to examine their behavior over the past decade. Between 2014 and 2021, India was one of the favorite destinations for global capital. Economic reforms such as GST, the Insolvency and Bankruptcy Code, corporate tax reductions and digital infrastructure development strengthened investor confidence. The Covid-era liquidity boom further accelerated inflows as central banks around the world injected trillions of dollars into financial markets.

However, foreign investors have always been highly sensitive to valuation and global liquidity conditions. Whenever India’s growth prospects improved while valuations remained reasonable, FIIs invested aggressively. Conversely, whenever valuations became stretched or global opportunities appeared more attractive, they reduced exposure. The pattern has remained remarkably consistent over the years. The current selling cycle appears to be another manifestation of this behavior rather than a fundamental rejection of the India growth story.

Why Are FIIs Selling Indian Equities?

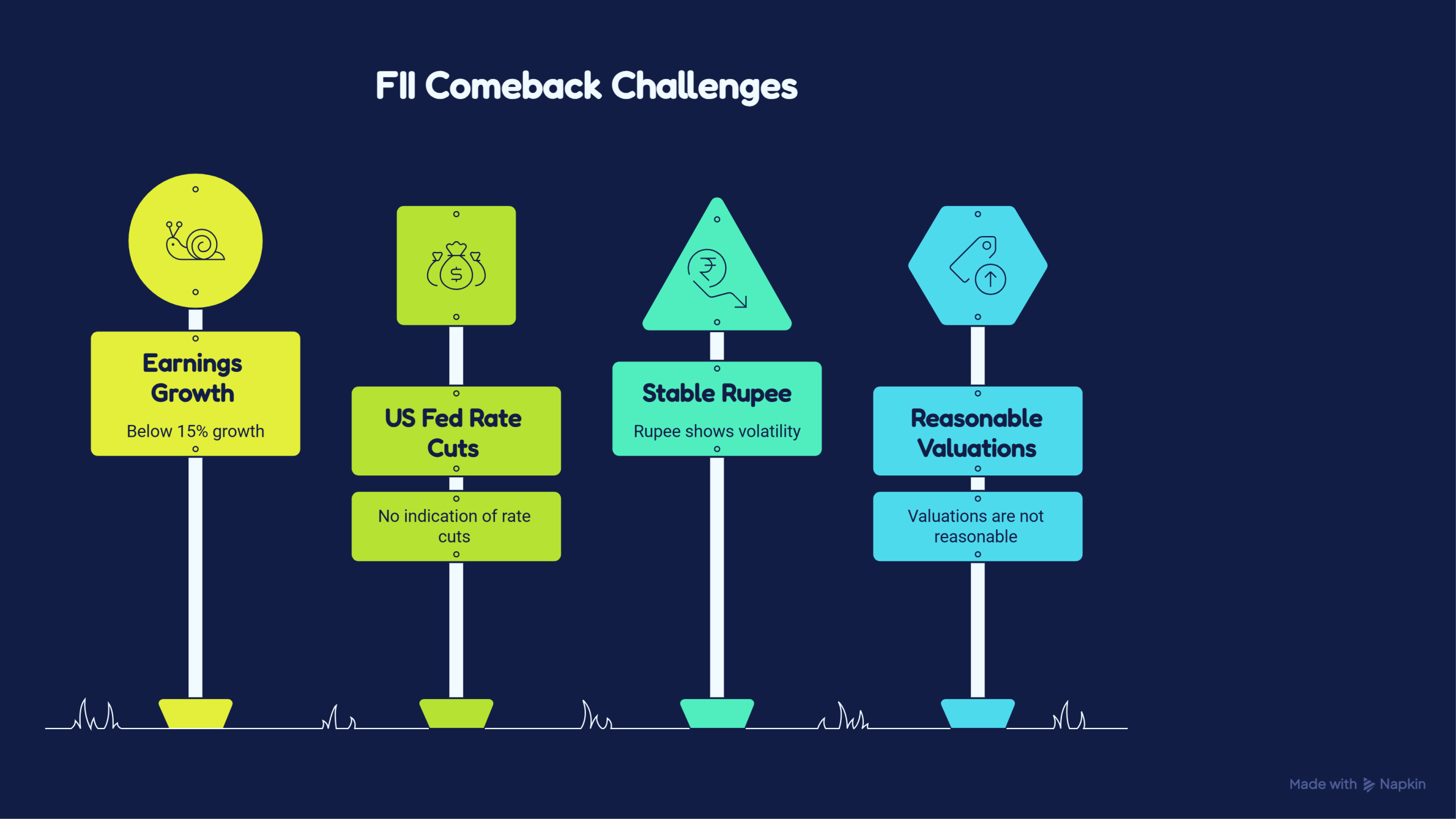

One of the most important reasons behind FII selling is valuation. India continues to command a significant premium compared with most emerging markets. While a premium valuation is justified for a faster-growing economy, many foreign investors believe that current prices already reflect several years of future growth. Markets such as China, South Korea, Taiwan and parts of Southeast Asia offer comparable opportunities at considerably lower valuations. For global fund managers allocating capital across dozens of countries, valuation remains a decisive factor.

Another reason is the moderation in corporate earnings growth. Over the past few years, investors expected Indian companies to deliver exceptionally strong profit growth. While corporate earnings have continued to expand, the pace has been slower than what market valuations appear to imply. As expectations and reality diverge, investors naturally become more cautious. This is particularly true for foreign investors who have alternative investment opportunities across the world.

The Impact of US Interest Rates and Dollar Strength

No discussion about FII flows can be complete without mentioning the United States. The aggressive interest rate hikes undertaken by the US Federal Reserve since 2022 have fundamentally altered global capital flows. For much of the previous decade, investors had little choice but to seek returns in riskier assets because interest rates in developed markets were near zero. Today, US Treasury securities offer attractive yields with significantly lower risk.

For a global investor, the decision becomes straightforward. If a relatively safe US government bond can generate competitive returns, the willingness to take additional risks in emerging markets naturally declines. This shift in the global risk-reward equation has played a major role in redirecting capital away from India and other emerging economies.

The Rupee Problem That Nobody Talks About

Foreign investors do not evaluate returns in rupees; they evaluate returns in dollars. This distinction is often overlooked in public discussions. Even if an investor earns double-digit returns in Indian equities, a weakening rupee can significantly reduce the effective return when converted back into dollars.

Over the past few years, the Indian rupee has remained under pressure because of higher crude oil prices, global uncertainty and portfolio outflows. Although the Reserve Bank of India has managed currency volatility reasonably well, persistent depreciation remains a concern for foreign investors. In many cases, currency losses can offset a substantial portion of equity gains, making other markets more attractive.

The AI Boom Has Changed Global Capital Flows

Another factor that has received less attention is the global artificial intelligence revolution. Taiwan and South Korea have become major beneficiaries of this trend because they host some of the world’s most important semiconductor companies. Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics and SK Hynix have emerged as key beneficiaries of the global AI boom.

As international investors seek exposure to artificial intelligence and advanced semiconductor manufacturing, capital has naturally flowed toward markets that offer direct participation in this theme. India has world-class software companies and a thriving digital ecosystem, but it currently lacks listed companies with the same level of global semiconductor dominance. This has resulted in a relative shift of capital toward competing Asian markets.

Is There a Policy Failure Behind the Outflows?

The temptation is to blame policy whenever foreign capital exits a market. However, the evidence suggests that India’s current challenges are largely cyclical rather than structural. India’s macroeconomic fundamentals remain stronger than many competing economies. GDP growth continues to outpace most major nations. The banking sector is healthier than it was a decade ago. Corporate leverage has declined significantly, and infrastructure investment remains robust.

That said, there is room for improvement. Investors frequently point to regulatory complexity, taxation uncertainty and limited market depth outside large-cap stocks as factors that reduce India’s competitiveness. These issues are not severe enough to trigger capital flight on their own, but they do influence investment decisions at the margin. In a world where capital can move instantly across borders, even small disadvantages matter.

What Will Bring FIIs Back?

The return of foreign investors will depend on a combination of domestic and global factors. First, corporate earnings growth must accelerate and justify current market valuations. Second, US interest rates must stabilize or begin declining, reducing the attractiveness of dollar-denominated assets. Third, the Indian rupee must remain relatively stable, reducing currency-related concerns. Finally, Indian valuations must become more competitive relative to other emerging markets.

History suggests that FIIs rarely stay away from India for long. They may reduce exposure during periods of valuation excess or global uncertainty, but they eventually return when risk-reward dynamics improve. The India growth story remains intact. What has changed is the price at which foreign investors are willing to participate in that story.

The Road Ahead

India’s fall from fourth to seventh place in global market capitalization rankings should not be interpreted as a crisis. However, it should be viewed as a warning. Economic growth alone is not sufficient to attract global capital indefinitely. Growth must translate into earnings, earnings must justify valuations, and policymakers must continue improving the ease of investing in India.

The good news is that India still possesses many of the ingredients that global investors seek: strong demographics, rising domestic consumption, expanding manufacturing capabilities and a growing digital economy. Foreign investors have not lost faith in India. They are simply demanding a more attractive entry point.

The real question, therefore, is not whether FIIs will return. History suggests they will. The more important question is whether India can use this period of foreign caution to strengthen its competitive position and reclaim its place among the world’s most valuable equity markets before the next wave of global capital arrives.