Vicky lived a complicated life.

On paper, he was a happily married man. His wife Koobs had stood beside him for years. But away from the legal and social structure of marriage, Vicky also maintained two romantic relationships — one with Loobs and another with Moobs.

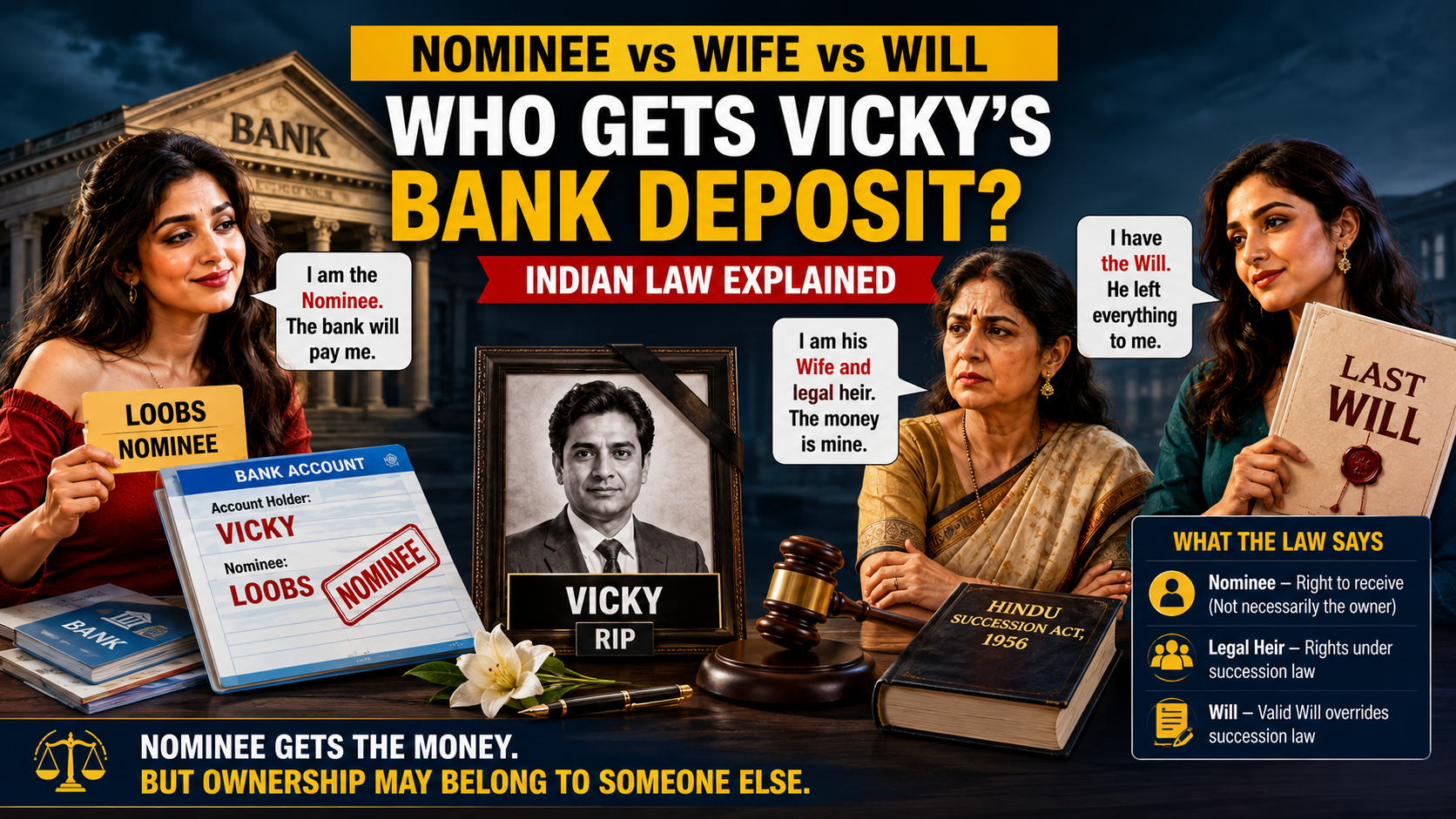

Like many financially aware urban Indians, Vicky maintained a sizeable bank deposit. One day, while trying to impress Loobs, he added her name as nominee in his bank account. Years later, fearing emotional drift in another relationship, he executed a carefully drafted Will leaving the same bank deposit to Moobs.

Then life took an unexpected turn.

Vicky died suddenly of natural causes. He left behind no children. Within days, all three women discovered the existence of the bank account.

Koobs, the lawful wife, claimed the money as Vicky’s legal heir under inheritance law.

Loobs marched into the bank armed with nomination papers and demanded immediate release of funds.

Moobs quietly produced a registered Will in which Vicky had specifically bequeathed the bank deposits to her.

Three women. One bank account. Three different legal claims.

So who really gets the money under Indian law?

The answer exposes one of the most misunderstood concepts in Indian banking and inheritance jurisprudence — the difference between a nominee, a legal heir, and a beneficiary under a Will.

The Great Indian Misconception About Nominees

Most Indians believe that a nominee automatically becomes the owner of money after the account holder’s death. This belief is reinforced because banks routinely release deposits to nominees without insisting on succession certificates or court orders.

But legally, nomination and ownership are two very different concepts.

Nomination in bank accounts is governed primarily by Section 45ZA of the Banking Regulation Act, 1949 read with the Banking Companies (Nomination) Rules, 1985. The provision allows a depositor to nominate a person who can receive the deposit after the depositor’s death.

The crucial point, however, is this: the law mainly protects the bank, not the nominee.

Section 45ZA effectively says that once a bank pays the nominee, the bank obtains a valid discharge of liability. In simple words, the bank cannot later be dragged into litigation by rival claimants because it acted according to nomination records.

But the provision does not conclusively declare the nominee as the final owner of the money.

That distinction changes everything.

RBI Rules: Convenience, Not Ownership

The Reserve Bank of India has consistently directed banks to simplify settlement of deceased deposit claims. RBI Master Directions on Customer Service encourage banks to promptly release money to nominees to avoid hardship for families.

From the banking system’s perspective, nomination is an administrative convenience mechanism. Banks are not expected to adjudicate inheritance disputes. They merely need a legally safe channel for payment.

This means Loobs, as nominee, can probably collect the money from the bank quickly. But receiving money from the bank is not the same as becoming the lawful owner of the money.

Ownership is determined separately under succession law and testamentary law.

What the Supreme Court Has Said

Indian courts have repeatedly clarified that nominees are generally trustees or custodians unless a statute specifically grants ownership rights.

The landmark Supreme Court judgment in Sarbati Devi v. Usha Devi (1984) became the foundation of this principle. Though the case dealt with life insurance, the Court clearly held that nomination does not override succession law. The nominee merely receives the amount for the benefit of those legally entitled to inherit.

The same reasoning has echoed across disputes involving shares, provident funds, and bank deposits.

More recently, in Shakti Yezdani v. Jayanand Jayant Salgaonkar (2023), the Supreme Court reaffirmed that nomination is primarily a mechanism for smooth transfer and not necessarily a mode of succession.

Thus, Loobs may receive the money initially, but her legal claim remains vulnerable if someone establishes a stronger succession right.

Enter the Most Powerful Instrument: The Will

The legal equation changes dramatically because Vicky executed a Will in favour of Moobs.

Under the Indian Succession Act, 1925, a Will is a legal declaration of intention regarding distribution of property after death. A valid Will generally overrides normal inheritance rules.

To be legally enforceable, a Will must:

- be signed by the testator,

- be executed voluntarily,

- be made while mentally sound,

- and be attested by two witnesses.

Under Hindu law, a person enjoys broad freedom to distribute self-acquired property through a Will. Vicky was therefore legally entitled to leave his bank deposits to anyone he wished — even a girlfriend.

Indian law may morally judge relationships, but testamentary freedom is remarkably wide.

That gives Moobs a potentially superior legal claim.

The Wife’s Rights Under Succession Law

Koobs, however, is not out of the picture.

As Vicky’s lawful wife, she is a Class-I heir under the Hindu Succession Act, 1956. If Vicky had died without a valid Will, she would ordinarily inherit his assets.

This creates the central legal conflict:

- the nominee claims through banking law,

- the wife claims through inheritance law,

- the girlfriend Moobs claims through testamentary law.

Among these three, Indian courts usually place the highest value on a valid Will.

So Who Ultimately Wins?

Practically, the bank will most likely release the money to Loobs because she is the registered nominee. The bank’s role ends there.

But once Moobs produces the Will, the dispute enters the realm of civil succession.

If the Will is proven genuine and legally valid, courts are likely to hold that Moobs is the beneficial owner of the deposit. In that event, Loobs may be legally compelled to transfer the money to Moobs despite having received it from the bank.

Koobs can still challenge the Will by alleging:

- fraud,

- coercion,

- suspicious circumstances,

- lack of mental capacity,

- or defective attestation.

If the Will collapses under judicial scrutiny, succession law revives. Since Vicky had no children, Koobs, as lawful wife, would likely inherit the deposit under the Hindu Succession Act.

In that scenario, even Loobs cannot retain the money merely because she was nominee.

The Larger Legal Lesson

The Vicky-Loobs-Moobs dispute captures a profound truth about Indian financial law:

A nominee is not necessarily an owner.

Nomination merely creates a payment channel. It does not automatically create inheritance rights.

The real battle is ultimately decided by succession law and testamentary intent.

In legal terms:

- the nominee gets the money from the bank,

- the legal heir gets rights under succession law,

- but the beneficiary under a valid Will often gets the strongest claim of all.

That is why estate planning experts repeatedly warn people not to confuse nomination with inheritance.

A nominee may hold the money.

But ownership may belong to someone else entirely.

#NomineeVsWill #LegalHeir #BankNominee #RBIRules #InheritanceLaw #IndianLaw #WillVsNominee #BankingLaw #SuccessionLaw #FinanceExplained #LegalExplainer #MoneyAfterDeath #EstatePlanning #IndianFinance #FingineerStory #SupremeCourt #LegalAwareness #BankAccount #Will #NomineeRules