SEBI’s proposal to extend Direct Market Access (DMA) to retail investors has generated excitement across the investing community. But before we celebrate another technological upgrade in India’s capital markets, there is a more important question worth asking—will this make retail investors better traders, or simply faster traders?

Every New Trading Feature Comes with a Promise. Does DMA Deliver?

“What does DMA mean for retail investors? Won’t it lead to overtrading and losing more money?”

That was my first reaction when I came across SEBI’s latest consultation paper proposing to extend Direct Market Access (DMA) to retail investors.

If you spend even a few minutes on social media, you’ll find people calling it a revolutionary move. Some believe brokers will become irrelevant. Others think brokerage charges will collapse. A few even claim that retail investors will finally get the same privileges as institutional traders.

The excitement is understandable. After all, who wouldn’t want access to a technology that has so far been reserved for large financial institutions?

But investing has taught us one important lesson: whenever something sounds revolutionary, it deserves careful examination.

The real question isn’t whether DMA is a good technology. The real question is whether it changes the way ordinary investors create wealth.

Understanding DMA Without the Technical Jargon

Imagine you decide to buy shares of Reliance Industries through your broker’s mobile application.

Most investors assume that the moment they press the “Buy” button, the order immediately reaches the stock exchange.

In reality, that isn’t how the process works.

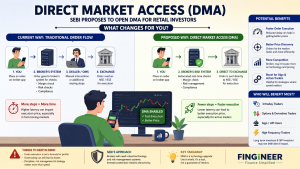

Your order first reaches your broker’s systems. Before it is allowed to enter the exchange, several automated checks take place. The broker verifies whether you have enough funds, whether sufficient margin is available, whether the order complies with regulatory limits and whether it satisfies various risk management parameters. Only after these checks are completed does the order finally reach the exchange for execution.

Direct Market Access doesn’t eliminate these safeguards.

Instead, it simplifies the routing process.

Under DMA, your order is electronically transmitted directly into the exchange’s trading system through the broker’s infrastructure after automated risk validation, without any manual dealer intervention.

Think of it as choosing an express lane at a toll plaza. You still pay the toll. Your vehicle is still inspected if necessary. But you spend less time waiting in traffic.

That, in simple terms, is what DMA seeks to achieve.

Why Is SEBI Thinking About This Now?

Timing is important.

When DMA was originally introduced in India, retail investing looked very different. Online trading was still evolving, internet speeds were slower and brokers relied far more on manual intervention than they do today.

Fast forward to 2026.

India has become one of the world’s fastest-growing retail investing markets. Discount brokers process millions of transactions every day. Real-time risk management systems have become highly sophisticated. Algorithmic trading is no longer limited to a handful of institutions.

In other words, the technology that once justified restricting DMA to institutional investors has evolved dramatically.

SEBI now believes that the infrastructure is mature enough to consider extending the facility to retail investors while continuing to protect market integrity through automated risk controls.

The proposal is therefore less about giving retail investors a special privilege and more about modernising India’s market infrastructure.

If DMA Is So Good, Why Was It Reserved for Institutions?

This is perhaps the most obvious question.

The answer lies in the nature of institutional trading.

A mutual fund purchasing shares worth ₹500 crore cannot afford delays in execution. A foreign institutional investor entering a large position wants every possible millisecond advantage. Algorithmic trading firms build strategies where execution speed itself becomes part of the edge.

For these participants, faster order routing directly translates into better execution quality.

That is why DMA has traditionally been used by mutual funds, insurance companies, foreign portfolio investors, proprietary trading firms and high-frequency traders.

They are not using DMA because it predicts the market.

They use it because it executes their decisions more efficiently.

That distinction is extremely important.

DMA helps execute a strategy.

It does not create one.

Does This Mean Brokers Will Become Redundant?

Probably the biggest myth surrounding the proposal is that brokers will disappear.

Nothing could be further from the truth.

Even if SEBI eventually allows retail investors to access DMA, brokers will continue to remain at the heart of the trading ecosystem.

They will still perform margin validation. They will still carry out automated risk checks. They will remain responsible for regulatory compliance, client reporting, surveillance obligations and settlement processes.

The only thing that changes is the route your order takes.

The broker doesn’t disappear.

The unnecessary delay does.

In fact, brokers may need to invest even more in technology, cybersecurity and risk management if they decide to offer DMA to retail clients.

Will Brokerage Charges Finally Come Down?

Another expectation that deserves a reality check is brokerage.

Many investors assume that because DMA reduces order routing delays, brokerage charges will automatically fall.

Unfortunately, the relationship isn’t that simple.

Brokerage depends on a broker’s business model, operating costs and competitive strategy—not merely on the technology used to route an order.

Globally, DMA is often marketed as a premium service because maintaining ultra-low-latency infrastructure requires significant investment.

Some Indian brokers may include DMA within their existing offerings. Others may reserve it for active traders or premium clients.

Competition could certainly improve pricing over time, but expecting DMA to eliminate brokerage would be unrealistic.

Who Is Likely to Benefit the Most?

This is where the excitement begins to separate from practicality.

For an investor who buys quality companies every month through a SIP and plans to hold them for ten years, DMA is unlikely to change life in any meaningful way.

Whether your order reaches the exchange in five milliseconds or thirty milliseconds has almost no impact on long-term wealth creation.

The real beneficiaries are likely to be traders whose strategies depend on execution quality.

Intraday traders, derivatives traders, scalpers, algorithmic traders and API-based trading users operate in an environment where even tiny delays may influence execution prices.

For them, DMA can improve efficiency.

For the average investor, however, the difference may hardly be noticeable.

This is not a criticism of DMA.

It is simply an acknowledgement that different tools serve different purposes.

Could DMA Encourage Overtrading?

Now we come to what may be the most important question of all.

Technology has a habit of making everything easier.

Sometimes that is a blessing.

Sometimes it becomes a temptation.

Retail investors already struggle with behavioural biases. Many confuse activity with productivity. They believe placing more trades somehow increases the probability of making money.

Experience tells us exactly the opposite.

The investors who constantly buy and sell often underperform those who remain patient and disciplined.

DMA cannot solve this problem.

In fact, by making execution even faster, it could unintentionally encourage some investors to trade more frequently than they should.

The uncomfortable truth is that most retail investors don’t lose money because their orders are slow.

They lose money because they chase momentum, ignore risk management and allow emotions to influence investment decisions.

No amount of technology can compensate for poor discipline.

What Do Existing DMA Users Say?

Institutional investors and professional trading firms have been using DMA for years, and their feedback is remarkably consistent.

They appreciate lower latency, more reliable execution and greater automation.

Interestingly, none of them claim that DMA guarantees profits.

Professional traders understand something that beginners often forget.

Execution quality matters only after a sound trading decision has already been made.

A perfectly executed bad trade is still a bad trade.

DMA can improve efficiency.

It cannot improve judgment.

What Should Retail Investors Take Away from This Proposal?

Viewed objectively, SEBI’s proposal is a positive development.

It reflects the regulator’s confidence in India’s technological capabilities and its willingness to democratise sophisticated market infrastructure.

But investors should resist the temptation to view DMA as a shortcut to higher returns.

Successful investing has never depended on who owns the fastest technology.

It has always depended on who exercises the greatest patience.

Whether you invest through a basic trading application or through an institutional-grade DMA platform, your long-term success will still depend on choosing good businesses, managing risk wisely and allowing the power of compounding to work over time.

Technology Evolves. Investment Principles Don’t.

SEBI’s proposal to extend Direct Market Access to retail investors marks another important milestone in the evolution of India’s capital markets. It is a sign that Indian market infrastructure is becoming increasingly sophisticated and globally competitive.

Yet perhaps the biggest lesson hidden within this proposal has nothing to do with technology.

Markets reward discipline far more consistently than speed.

DMA may help your order reach the exchange a few milliseconds earlier, but it cannot teach patience, eliminate greed or prevent emotional decision-making.

Retail investors should certainly welcome technological progress. Better infrastructure ultimately benefits everyone.

But before asking whether your trades will become faster, it may be worth asking a far more important question:

Will your investment decisions become better?

Because in the end, that—not execution speed—is what determines long-term wealth creation.