A strong regulator doesn’t always need to shout to be heard. The recent listing process of NSDL (National Securities Depository Limited) is a prime example of the silent effectiveness of India’s capital markets watchdog — the Securities and Exchange Board of India (SEBI).

The announcement of the NSDL IPO price band came as a shock to grey market speculators, catching them completely off guard. The IPO price band was far below expectations, and as a result, speculative activity in the unlisted shares of NSDL came to a grinding halt. The market that was beginning to resemble a casino suddenly froze. With major upcoming listings like NSE still in the pipeline, the unlisted market is now treading cautiously. Let’s unpack the situation in detail.

Understanding the Unlisted Market

Unlisted company shares are traded on informal platforms before the company goes public. Shareholders receive shares in demat form and can sell them to willing buyers — often years before an IPO. These shares are typically traded in predefined lots.

Take the example of the National Stock Exchange (NSE). Its shares have been trading in the unlisted market for the past four years, typically in lots of 250 shares. Investors can’t buy less than one lot and must buy in multiples. Just like in the listed market, unlisted shareholders receive dividends and bonuses and react to news flows.

The NSE shares have seen a 52-week range from ₹1,600 to ₹6,200 — an eye-popping range for a stock with just ₹1 face value. Hopefully, this gives a basic sense of how the unlisted space functions.

What Changed Overnight?

While the unlisted market isn’t new, recent developments have exposed its vulnerabilities — particularly the loosely regulated grey market.

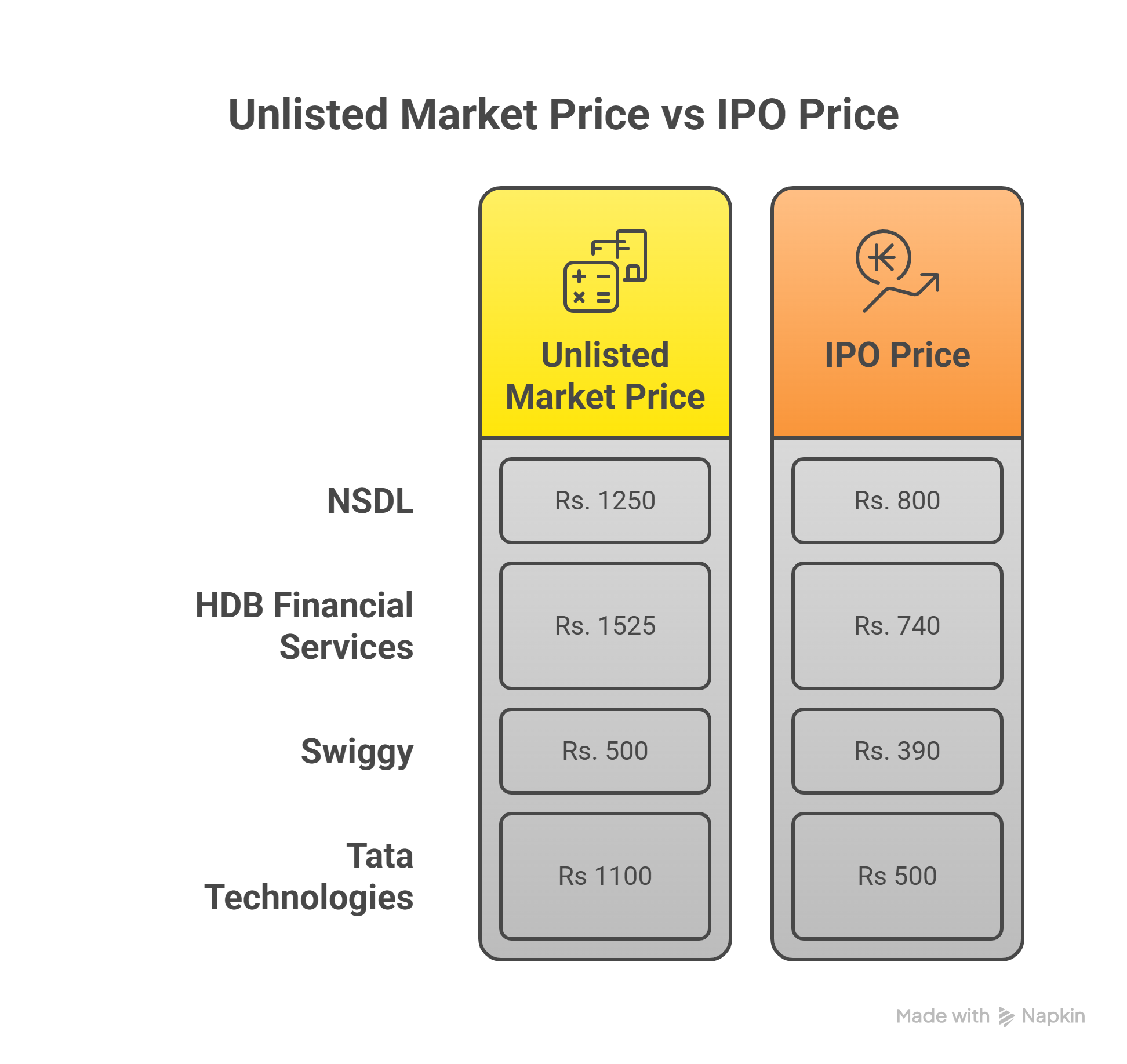

In the grey market, investors can “pre-book” shares of an upcoming IPO by paying just 10–20% of the expected listing price. These deals are often driven by hype, not fundamentals. In the case of NSDL, its unlisted shares were trading at ₹1,250 — based on a rough comparison with peer company CDSL, which was trading near ₹1,600.

Investors were anticipating a 25–30% premium on the IPO listing over the unlisted price. But SEBI had other plans. The IPO was announced with a price band of ₹760–₹800 — nearly 35% lower than the grey market’s assumed price of ₹1,250.

Speculators who had already locked in pre-IPO deals at around ₹1,600 — expecting 40% gains — suddenly found themselves staring at losses. The grey market, built on anticipation and leverage, was thrown into disarray.

How the Grey Market Works (and Fails)

Let’s break it down with an example:

Imagine a company, ABC Ltd., is coming out with an IPO at ₹1,000 per share. The grey market is trading it at ₹1,200 — a 20% premium. You have ₹2 lakh and want to invest but fear missing out on IPO allotment.

Instead, you go to the grey market and “book” 1,666 shares at ₹1,200. If the stock lists at ₹1,400, you make a neat ₹3.33 lakh profit. But if it lists at ₹1,100, you’re down by ₹1.66 lakh. It’s high-risk, high-reward — or in this case, high-speculation.

This is what happened with NSDL — the listing price surprise completely unraveled speculative bets.

A Regulator’s Wake-Up Call

The NSDL case isn’t isolated. Several IPOs in recent times have been priced strategically to combat grey market manipulation. SEBI seems determined to bring order to the chaos.

Whether it’s rationalizing IPO pricing, increasing transparency, or recent reforms in the derivatives segment, the regulator’s steps aim to create a more level playing field — one where informed investment is rewarded over blind speculation.

The NSDL episode is a clear message: the days of unchecked speculation are over. SEBI’s quiet but firm interventions are reshaping market behavior — and that deserves recognition.

Final Thoughts

The Indian capital markets are evolving — and so is the regulatory ecosystem. While grey markets won’t disappear overnight, their influence is waning. A smarter, more vigilant regulator is taking charge, and that’s a positive sign for long-term investors.