The sudden 50% intraday surge in the US-listed American Depository Receipt (ADR) of Infosys (on 19th December 2025) was not just a market oddity. It was a stress test — and one that exposed gaps in how cross-border market dislocations are understood, communicated and regulated.

For a large, fundamentally stable Indian IT major, such a move cannot be explained by business performance. There was no earnings shock, no strategic announcement and no corresponding movement in the India-listed shares. What moved the price was not information, but compulsion — forced buying driven by market structure.

For regulators and policymakers, that distinction matters.

When markets move without information

Financial markets are built on the idea of price discovery. But in episodes like this, prices are not discovered — they are produced by mechanical stress.

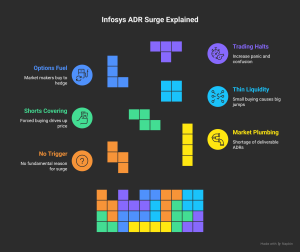

The Infosys ADR spike bears the hallmarks of a classic squeeze scenario: constrained share availability, forced short covering, thin liquidity and possible amplification from options hedging. Once such dynamics begin, prices can detach rapidly from fundamentals.

That the exchange had to invoke multiple volatility halts underlines the point. These safeguards are designed to slow disorderly trading, not to validate the move itself.

Yet for retail investors watching from the sidelines, the absence of clear, timely explanations creates confusion. In that vacuum, speculation thrives.

Cross-border listings, asymmetric risk

This episode highlights a structural asymmetry. Indian companies with overseas listings expose domestic investors to offshore volatility that originates outside India’s regulatory perimeter, yet spills back into domestic sentiment.

While the ADR market is regulated by US authorities, the reputational and confidence impact lands squarely in India. Indian regulators cannot intervene directly in ADR trading, but they are not powerless either.

The problem is not jurisdiction. It is communication.

A silence problem, not a rulebook problem

India’s regulatory framework is not weak. SEBI’s surveillance mechanisms, prohibitions on manipulative practices and circuit filter systems are robust by global standards. The issue is not the absence of rules, but the absence of rapid, coordinated disclosure when abnormal events occur abroad.

When a widely held Indian stock experiences a violent offshore dislocation, three parties are best placed to respond quickly:

- the issuer,

- the domestic exchange, and

- the depository or intermediaries involved in cross-listing.

A simple, factual clarification — confirming whether there is any material information, settlement issue, or corporate trigger — would go a long way in preventing misinformation and panic-driven trading.

In the Infosys case, the lack of immediate, authoritative explanation allowed rumours to fill the gap.

The limits of investor protection

It is also important to be clear about what regulation can and cannot do.

Investor protection mechanisms are designed to safeguard against fraud, mis-selling and intermediary failure. They do not, and cannot, protect investors from price volatility driven by leverage, derivatives or short-term trading strategies.

Retail investors who chase sudden price spikes often misunderstand this distinction. They assume that if a stock is “regulated”, its price must be rational. Episodes like this prove otherwise.

Policy lessons worth considering

The Infosys ADR episode offers several actionable lessons:

First, regulators should develop a formal cross-border volatility response protocol for major Indian issuers. This need not involve intervention, only timely disclosure and coordination.

Second, greater aggregate transparency around stock lending stress — without naming participants — could help markets assess squeeze risk more rationally.

Third, surveillance frameworks must explicitly integrate derivatives positioning and hedging feedback loops, which increasingly drive extreme short-term moves.

Finally, investor education efforts should focus less on returns and more on market mechanics — explaining that not all price moves reflect value, and that forced buying is inherently unstable.

A market signal policymakers should not ignore

The Infosys ADR spike was not a failure of markets, nor a scandal. But it was a reminder that modern markets are complex, interconnected and occasionally fragile.

For policymakers, the real risk is not volatility itself, but the erosion of trust that follows unexplained volatility.

Silence, in such moments, is costly.

If India aspires to deepen its capital markets and attract long-term household participation, it must ensure that when markets behave abnormally — even outside its borders — investors are not left guessing.

Because in markets, uncertainty travels faster than truth.