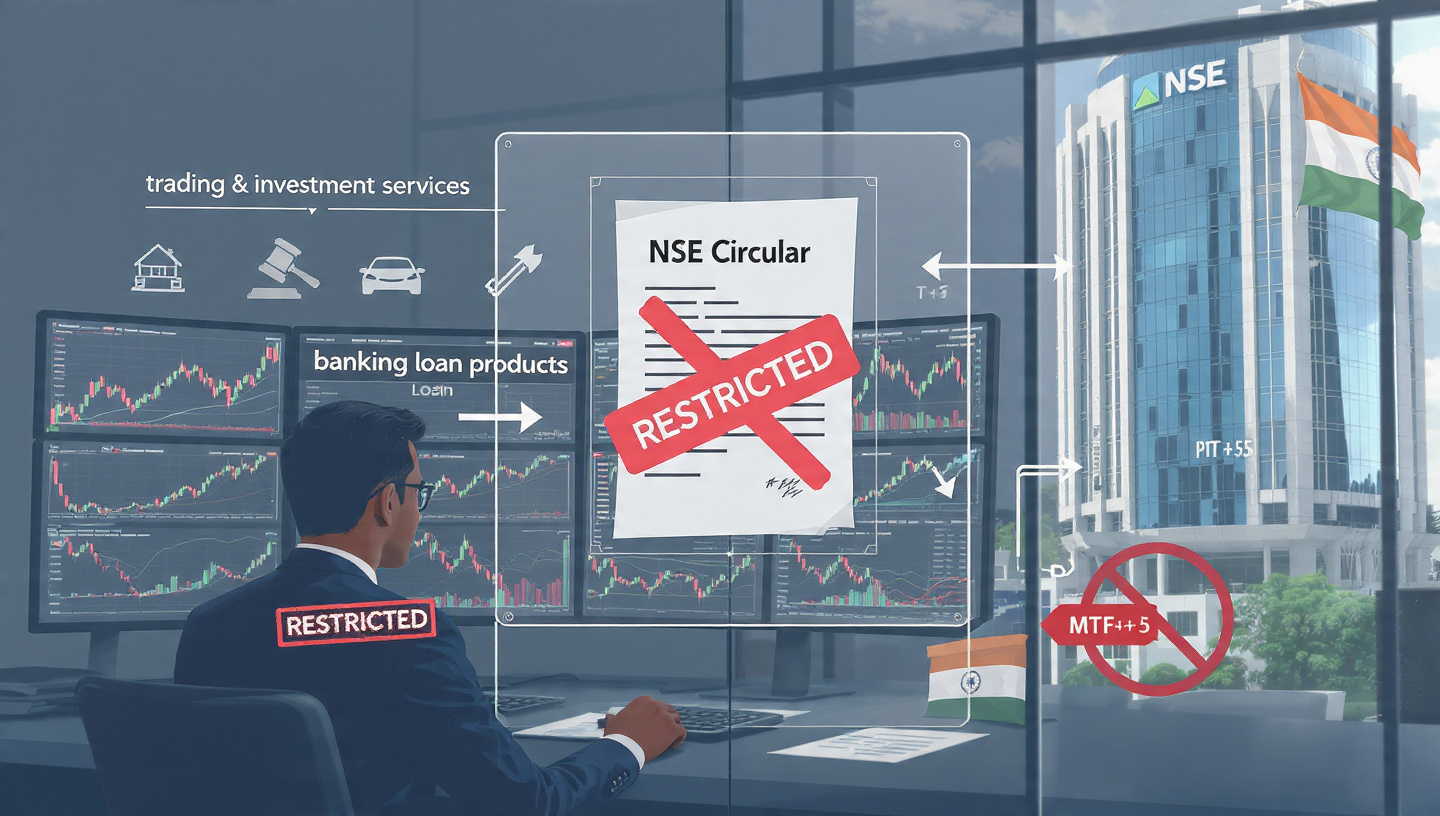

The National Stock Exchange (NSE) has drawn a firm regulatory boundary for stock brokers, prohibiting them from distributing or offering banking loan products, even if such entities are also registered as research analysts (RAs). The directive, issued through a circular earlier this week, reinforces the exchange’s June 2025 framework on third-party product distribution and signals a tightening of oversight amid the growing convergence of brokerage, advisory and retail lending activities. The exchange said it had observed instances of trading members actively distributing banking loan products—an activity that falls outside the regulatory framework governing stock brokers.

What the Circular Says

In unequivocal terms, the NSE clarified:

“Stock brokers are not permitted to engage, as distributors, in any lending products other than those specifically permitted by SEBI from time to time.”

Currently, the only lending products permitted for distribution by brokers are:

- Margin Trading Facility (MTF)

- T+1+5 funding

All other banking loan products—including home loans, personal loans, vehicle loans, education loans and loans against securities—are expressly prohibited. Crucially, the exchange made it clear that these restrictions apply regardless of any additional registration held by the broker.

“The exchange’s framework prevails for trading members irrespective of any additional registrations,” the circular said.

This clarification effectively shuts the door on arguments that parallel registrations or group-level structures could allow brokers to engage in banking product distribution.

Why the Clarification Was Necessary

The circular follows FAQs issued by the Securities and Exchange Board of India (SEBI) in July 2025 on research analyst regulations, which stated that research analysts may distribute non-SEBI products—such as banking products—at a family or group level, with grievances relating to such distribution falling outside SEBI’s jurisdiction. Market participants say some brokers interpreted these FAQs expansively, relying on dual registrations to justify the cross-selling of banking loan products to their trading clients. The NSE’s intervention makes it clear that exchange-level obligations applicable to trading members cannot be diluted by additional registrations. At a broader level, the exchange appears concerned about regulatory arbitrage and the steady blurring of lines between execution, advisory and lending—particularly on digital platforms that integrate multiple financial services into a single interface.

Implications for Investors

From an investor protection perspective, the move is largely preventive.

Allowing brokers to simultaneously facilitate trading and distribute loan products heightens the risk of conflicts of interest. Even without explicit misrepresentation, such arrangements can influence investor behaviour, subtly encouraging leverage or normalising borrowing as part of routine market participation. By enforcing a clear separation between investment services and banking loan distribution, the NSE reduces the scope for mis-selling and ensures that borrowing decisions remain independent of trading or advisory interactions. The move also helps contain leverage-driven risks in the retail segment, which tend to build up during bullish market cycles and amplify losses during corrections.

Impact on Brokers and Business Models

For brokers, the circular has immediate operational implications.

Entities that had entered into referral or distribution arrangements with banks and non-bank lenders will need to unwind such partnerships. The NSE has advised trading members to review their business models, marketing practices, app interfaces and third-party tie-ups to ensure strict compliance. While the restriction may affect certain ancillary revenue streams, it also narrows the scope of permissible activities to clearly defined functions—trading, execution, advisory within registration limits, and SEBI-approved financing. In regulatory terms, this reduces ambiguity and long-term compliance risk. Market participants note that the directive may disproportionately affect brokers that had positioned themselves as full-stack financial platforms, rather than pure-play market intermediaries.

Concerns Around Leverage and Mis-Selling

The NSE circular does not cite specific enforcement cases. However, the regulatory concern is rooted in well-documented market behaviour.

Historically, periods of heightened retail participation—both in India and globally—have coincided with increased borrowing, often facilitated by easy credit access and platform-driven nudges. Regulators have consistently emphasised that mis-selling can arise not only from false claims but also from conflicted incentives, product bundling and inadequate risk disclosure. The NSE’s intervention appears aimed at addressing these risks pre-emptively, rather than reacting after investor harm or market stress has materialised.

A Clear Regulatory Signal

Beyond its immediate scope, the circular sends a broader message to the market. Exchange oversight applies fully to trading members, regardless of additional registrations or group-level structures. Functional boundaries within the financial ecosystem, the NSE has signalled, are not optional. By reasserting these limits, the exchange has sought to refocus brokers on their core market roles at a time when retail participation is expanding and product innovation is accelerating.