Sometimes, a sentence can be worth ₹15,000 crore in market capitalization. It can change the way traders look at risk, alter the future revenue expectations of exchanges, and move money—real money—within minutes. On November 7, 2025, one such sentence was spoken.

At a leadership forum in Mumbai that morning, SEBI Chairperson Tuhin Kanta Pandey was asked whether the regulator was considering curbs on weekly Futures & Options (F&O) contracts, a subject that has animated trading desks and retail strategy groups for months. The Chair smiled lightly before responding:

“The current certainty is that weekly F&O is on.”

There was no policy change. No circular followed. No discussion paper was issued. Yet the market reacted as if one of the most consequential decisions in exchange economics had just been announced.

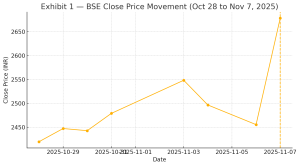

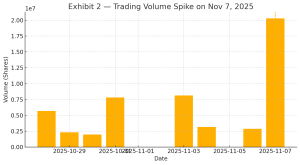

Within minutes, BSE Ltd. began to surge. By the close of trade, the stock was up around 9%, ending near ₹2,678 after touching an intraday high of ₹2,718.70. The volume was even more striking: from roughly 2.9 million shares the previous day to more than 20 million. The regulator had not changed the rules, yet the market moved to the regulator’s voice.

The upward spike on November 7 stands out sharply against the prior period’s stability. This was not a corporate development story. It was a policy-interpretation story.

India runs one of the world’s most derivatives-driven equity markets. More than 95% of daily derivatives volume comes from index options trading, much of it retail or pseudo-retail, routed through discount brokerages, advisory channels and automated strategy platforms. Weekly expiry volume has become, effectively, the flywheel of revenue for exchange trading operations.

Because NSE is not listed and BSE is, BSE’s stock has become the real-time sentiment gauge for regulatory tone around weekly derivatives.

When regulators caution, BSE tends to fall.

When regulators reassure, BSE tends to rise.

The surge indicates participation across trading categories: institutional desks, algorithmic liquidity providers, proprietary books and retail momentum accounts.

The intraday reaction followed a familiar sequence: First, the statement circulated on broadcast. Then caption feeds parsed the language. Algorithmic systems trained on tone-recognition patterns began buying. Futures moved first, and spot prices aligned through arbitrage channels. Option writers hedging gamma exposure then accelerated the upside momentum. Retail traders arrived last, reacting to social and media commentary. There was no sign of manipulation or privileged access. The structure of the market responded to the signal contained in the statement.

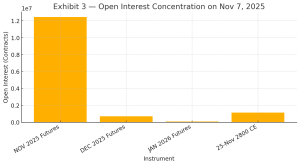

Open interest in near-term BSE futures stood around 12.45 million contracts, far outweighing later maturities. A heavily traded 2800 strike call option also carried significant open interest. This indicates that the market treated the statement as short-horizon directional clarity, not a long-term valuation shift.

This was not the first instance of regulatory tone influencing exchange stock pricing. Under SEBI Chairperson Madhabi Puri Buch, remarks on retail derivatives risks in 2023–24 triggered temporary declines in BSE and brokerage ecosystem stocks such as Angel One and Motilal Oswal. During the transition to the current administration, uncertainty itself became a priced asset.

The core issue here is not whether weekly F&O is good or bad for retail investors. It is not whether speculation is excessive. It is not whether retail risk appetite needs to be restrained.

The core issue is communication structure.

In a derivatives-led market, where pricing adjusts faster than speech spreads, when a regulatory figure speaks during live market hours, words move capital.

This is not a moral problem. It is a timing problem.

A More Neutral Communication Architecture

India would not be the first jurisdiction to adjust communication strategy. Market-moving institutions already follow structured regimes:

| Institution | Practice |

|---|---|

| US Federal Reserve | Scheduled statements + embargoed press notes |

| ECB | Pre-announced briefings + synchronized transcript releases |

| UK FCA | Policy commentary generally after market hours |

There is no loss of authority in structure — only equal access to interpretation.

A few low-friction adaptations:

- Release policy-sensitive remarks after 3:30 PM

- Use pre-published Q&A frameworks for regulated-entity speeches

- Provide simultaneous public text release with televised remarks

- Avoid open-ended policy speculation in conversational broadcast settings

These suggestions do not constrain the regulator.

They simply level the timing of signal reception.

The reaction on November 7, 2025 revealed that the market has evolved faster than the communication norms surrounding it. When expectations trade faster than decisions, the words used to describe decisions become part of the market. The regulator did not intend to move BSE that day. But speech now carries the weight that circulars once did. In a derivatives-heavy market, communication is no longer commentary. It is capital flow.

Sometimes, a sentence really can be worth ₹15,000 crore.

#IndianMarkets #SEBI #BSE #Derivatives #MarketPolicy #RegulatorySignals #StockMarketIndia #MarketMicrostructure #FinancialRegulation