The mutual fund industry in India is witnessing unprecedented growth, largely driven by retail investors. Systematic Investment Plans (SIPs) have become a household investment tool, contributing to the sharp rise in mutual fund Assets Under Management (AUM), which stood at ₹74.79 lakh crore as of June 2025. The number of mutual fund folios has surged to 17.79 crore in FY 2023–24. Alarmingly, over 99% of these folios—17.68 crore—are held by retail investors (individuals and HUFs), placing small investors at maximum risk. The provision for investing without a Permanent Account Number (PAN) has further amplified this vulnerability.

The Rise of Retail in Mutual Funds

Regulated by the Association of Mutual Funds in India (AMFI) and the Securities and Exchange Board of India (SEBI), mutual funds require stricter Know Your Customer (KYC) compliance than bank accounts. Despite these safeguards, the number of unique PAN-linked mutual fund accounts has grown from 1.25 crore in March 2017 to 4.97 crore in March 2024.

This rapid growth is fueled by strong post-COVID returns, aggressive marketing by AMFI, and social media narratives promising massive wealth through SIPs. The launch of ₹250 SIPs has opened the door for investors from Tier-3 cities and rural regions. While this democratization of investing is commendable, it also concentrates risk among financially vulnerable groups who may not fully understand the implications of their investments.

The Danger of Folio Concentration

The concentration of over 99% of mutual fund folios in the hands of retail investors creates a precarious situation. A market correction, regulatory misstep, or scheme failure could trigger panic, leading to large-scale redemptions. Such a shock would destabilize not just the mutual fund sector, but potentially the broader capital markets as well. Retail investors would be hit hardest, while the cascading effect could strain the liquidity and stability of the financial ecosystem.

The PAN Exemption Loophole

The continued allowance of PAN-exempt investments, despite tightened KYC norms, raises concerns. While intended to boost mutual fund penetration in underserved areas, this provision may inadvertently enable benami transactions and facilitate money laundering.

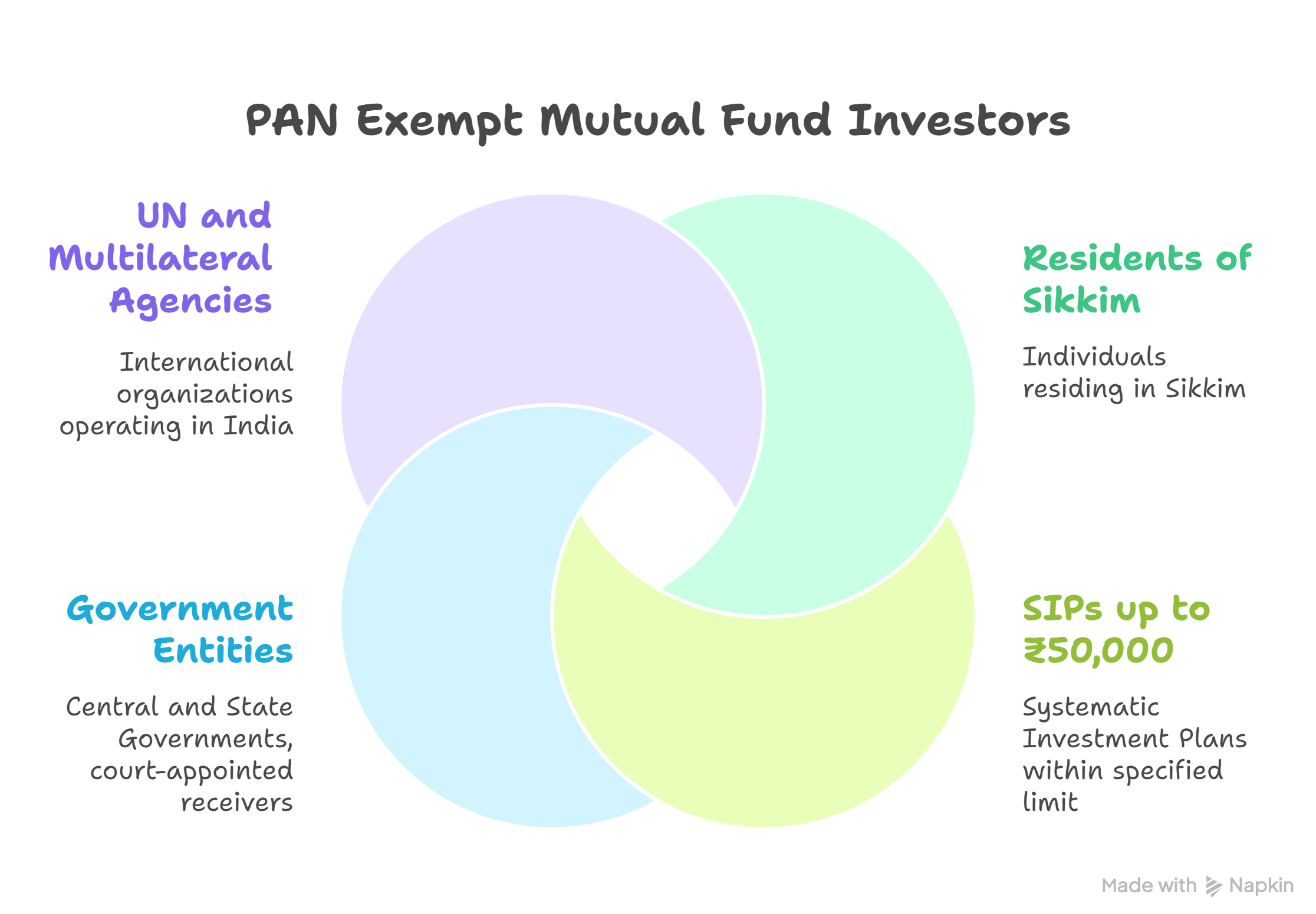

Currently, the following categories are exempt from PAN requirements for mutual fund investments:

- Residents of Sikkim

- SIPs up to ₹50,000 per financial year

- Central and State Governments, court-appointed receivers or liquidators

- UN and multilateral agencies operating in India

These investors are issued a PAN Exempt KYC Reference Number (PEKRN). However, data from AMFI shows that only 3.5 lakh such investors existed as of March 2024. This limited number suggests that the exemption has had minimal impact on financial inclusion. In contrast, the existence of 60.3 lakh demat accounts under PAN-exempt status points to possible misuse (money laundering and benami investment).

The ₹250 SIP: A Double-Edged Sword

The launch of ₹250 SIPs by former SEBI Chairperson Madhabi Puri Buch was seen as a landmark moment for financial inclusion. However, it has also exposed a vulnerable section of society to market risks they may not fully understand. Many of these small investors are driven by social media influencers promoting unrealistic wealth creation stories. Their lack of financial literacy makes them easy targets for mis-selling and misinformation.

App-based platforms offering PAN-exempt investing, such as Paytm, may improve accessibility but pose significant systemic risks. The memory of the US-64 debacle involving Unit Trust of India still looms large—then, it was a single fund. Today, with 45 AMCs managing over 2,500 mutual fund schemes, the scale of potential damage is far greater.

A Call for Responsible Regulation

Regulators must act with caution when expanding mutual fund access to semi-urban and rural areas. While inclusion is essential, it should not come at the cost of stability. Overzealous distribution, driven by attractive commissions and low financial literacy, could lead to rampant mis-selling.

The PAN exemption facility must be re-evaluated. Its limited utility in boosting participation and its potential misuse for benami and illegitimate transactions make it a liability in the long term.

Conclusion

India’s mutual fund revolution must be tempered with responsibility. As retail investors become the backbone of the industry, regulators and AMCs must prioritize their protection. Ensuring transparency, enforcing stricter compliance, and eliminating loopholes like the PAN exemption are crucial steps toward safeguarding the future of small investors—and the integrity of the financial system.